Business Owner Policy Insurance Quote

Introduction

Ambitious entrepreneurs launching new enterprises inevitably juggle multiple complex priorities from securing eager first customers to managing tricky cashflows in those delicate formative years. Yet a recurring obligation also deserves prompt attention – obtaining a business owner policy (BOP) insurance quote delivering consolidated protection from material mishaps.

This article provides a comprehensive guide to accessing business owner policy quotes encompassing suitable coverages, premium guidance, obtaining bids, comparing offerings and key questions.

Let’s explore tips to secure this vital shield against ruinous scenarios as an anxious new business operator.

Suitable Business Owner Policy Coverages

Nine core covers particularly useful for startups and SMEs commonly packaged within convenient BOPs include:

- Property insurance – shields owned premises and contents like equipment, stock from incidents like fire, storms etc.

- Business interruption – provides income replacement if property damage from insured events disrupts operations.

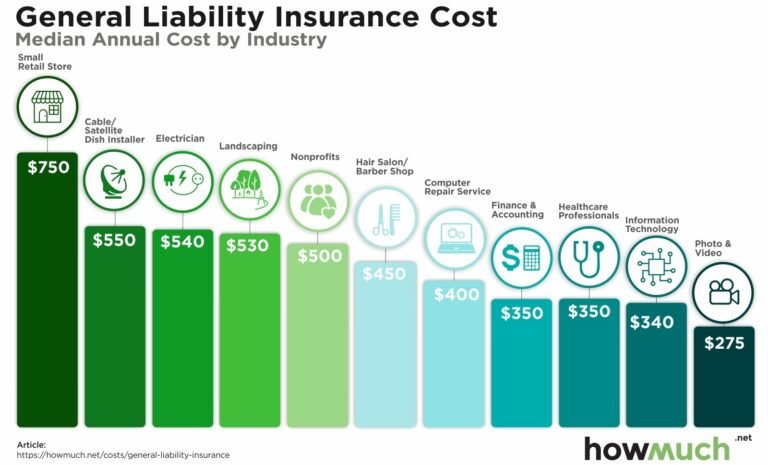

- General liability – covers legal claims if customers are injured because of business negligence.

- Commercial vehicles – mandatory auto insurance for cars, trucks, vans used for work.

- Commercial crime – protection from staff/external theft, fraud etc.

- Cyber insurance – responds to hacking incidents and data breaches causing harm.

- Directors and officers liability: Shields management decisions legally challenged.

- Employment practices liability: Protects against staff lawsuits over issues like wrongful dismissal.

- Workers compensation: Covers medical costs and compensation for staff injuries at work.

Bundling provides administrative ease and potential dollar savings over stand alone policies.

Premium Guidance

Indicative first year startup business owner policy premiums for core covers like property damage, liability and vehicle insurance could range from:

- Sole trader home based consulting or online businesses – $600 to $1000+.

- Small suburban professional services, retail shop or franchise – $1500+

- Larger regional SMEs with some manufacturing, machinery, fleet – $4000+

Final premiums reflect risk variables like business sector, location, revenue, claims histories etc.

Obtaining Business Insurance Quotes

New owners should:

- Clarify must have vs nice to have covers based on launch plans, staffing, locations. Review any minimum legal, contractual requirements already set by clients or industry bodies.

- Define estimations of key metrics insurers will request around property value, annual sales, payroll etc rather than responding with uninformed guesses unable to be validated later which could invalidate policies.

- Identify likely incumbent insurers based on local market presence and brands specialising in startups. Wider quote searches may be assisted by business advisors with commercial insurance experience.

- Use online quotation portals to instantly compare premium estimates across candidate providers – avoiding delays scheduling traditional in-person broker meetings at this busy juncture.

- Evaluate variances in pricing, cover inclusions and excesses to isolate the optimal value protection mix within set budget ceilings.

Comparing Business Insurance Offerings

Key variables to assess when judging multiple quotations include:

- Overall premium value: Balance against higher excesses possibly exposing business to bigger upfront incidental costs.

- Specific cover limits: Do maximum claim limits per section align to realistic business scale?

- Policy stability: Long standing insurers present lower risk of distressed withdrawal compared to new entrants.

- Claims processing ease: Review ratings for insurer claims handling responsiveness, digital lodgement options.

- Exclusions review: Ensure no unreasonable constraints on claim circumstances evident in Policy Product Disclosure Statements.

- Associated fees check: Beyond core premiums, look for extra charges around installment payments, administration etc.

Placing emphasis on broadly understanding key legal terminology in base policies seen empowers newly insured startups to best judge competing offerings.

5 Key New Business Owner Quotes Questions

- What is defined as ‘tools of trade’ requiring coverage? Equipment like laptops, tools and stock used in earning business income.

- Must new business insurance be taken out in the entity name? Yes – personal names don’t appropriately cover incorporated entities if claiming funds to offset company losses.

- Are quotes guaranteed or estimations? Indicative quotes provide likely premium costs that may be adjusted once fuller details supplied to underwriters. Firm quotes follow formal assessments.

- Can policies commence from a future date? Yes – buyers can nominate required commencement dates aligned with actual trading launch rather than when initially seeking quotes. Useful for forward planning.

- What is Professional Indemnity insurance? Covers advice givers against negligence claims and an essential addon for consultants.

Conclusion

Amidst the exhilarating entrepreneurial journey grappling daily with strategic imperatives that will make or break eventual prosperity aspirations, pausing temporarily to lock down fundamental business insurance shields against financially crippling mishaps makes smart leadership. Seeking multiple comparative quotations drives informed coverage selection balancing premium outlays against genuine exposures protection for recently established ventures. Consult experienced brokers for assisting overwhelmed founders determine adequate cover sweetspots their independent industry knowledge often reveals. Right-sized business owner policies ensure journey duration